IRS Audits

Here’s what you should know about an IRS audit:

- Usually, a taxpayer will only be subject to one audit per tax year.

- The IRS generally has three years from the date taxpayers file their returns to assess any additional tax for that tax year.

There are some limited exceptions to the three-year rule, including when taxpayers fail to file returns for specific years or file false or fraudulent returns. In these cases, the IRS has an unlimited amount of time to assess tax for that tax year.

- If following an audit, the IRS determines you owe additional taxes, you will receive a statutory notice of deficiency. This is a letter proposing additional tax the taxpayer owes. This notice must include the deadline for filing a petition with the tax court to challenge the amount proposed.

- The IRS normally has 10 years from the assessment date to collect unpaid taxes. This 10-year period cannot be extended, except for taxpayers who enter into installment agreements, or the IRS obtains court judgments.

There are circumstances when the 10-year collection period may be suspended. This can happen when the IRS cannot collect money due to the taxpayer’s bankruptcy or there’s an ongoing collection due process proceeding involving the taxpayer.

Source: IRS

Your Rights as a Taxpayer

In the event you need to work with the IRS on a personal tax matter including, but not limited to, filing a return, paying taxes, responding to a letter, going through an audit or appealing an IRS decision, you can expect the following rights:

1. The Right to Be Informed

2. The Right to Quality Service

3. The Right to Pay No More than the Correct Amount of Tax

4. The Right to Challenge the IRS’s Position and Be Heard

5. The Right to Appeal an IRS Decision in an Independent Forum

6. The Right to Finality

7. The Right to Privacy

8. The Right to Confidentiality

9. The Right to Retain Representation

10. The Right to a Fair and Just Tax System

Source: IRS Publication 1

IRS Free E-file for Those Who Make $72,000 or less

IRS Free File online products are available to any taxpayer or family whose adjusted gross income (or AGI) is $72,000 or less in 2020.

How IRS Free File Online works

The IRS Free File Program is a partnership between the IRS and many tax preparation and filing software industry leaders who provide their brand-name products for free as part of a 19-year partnership with the IRS. There are nine products in English and two in Spanish.

Traditional IRS Free File provides free online tax preparation and filing options on IRS partner sites. Each IRS Free File provider sets its own eligibility rules for products based on age, income and state residency. However, for those who make $72,000 or less, they will find at least one product that matches their needs, and usually more. Some providers also offer free state preparation.

For those whose income (AGI) is greater than $72,000 and know how to prepare their own tax return, they can use the Free File Fillable Forms.

For 2021, these providers are participating in IRS Free File:

• 1040Now,

• ezTaxReturn.com,

• FreeTaxReturn.com,

• FileYourTaxes.com,

• Intuit (TurboTax),

• On-Line Taxes (OLT.com),

• TaxAct,

• TaxHawk (FreeTaxUSA),

• TaxSlayer.

For 2021, the following providers have IRS Free File products in Spanish:

• ezTaxReturn.com,

• TaxSlayer (Available after January 18).

Source: IRS

How Much Americans Made in 2018 – Numbers Tell Stories Series – Part I

By AccountingGo Staff

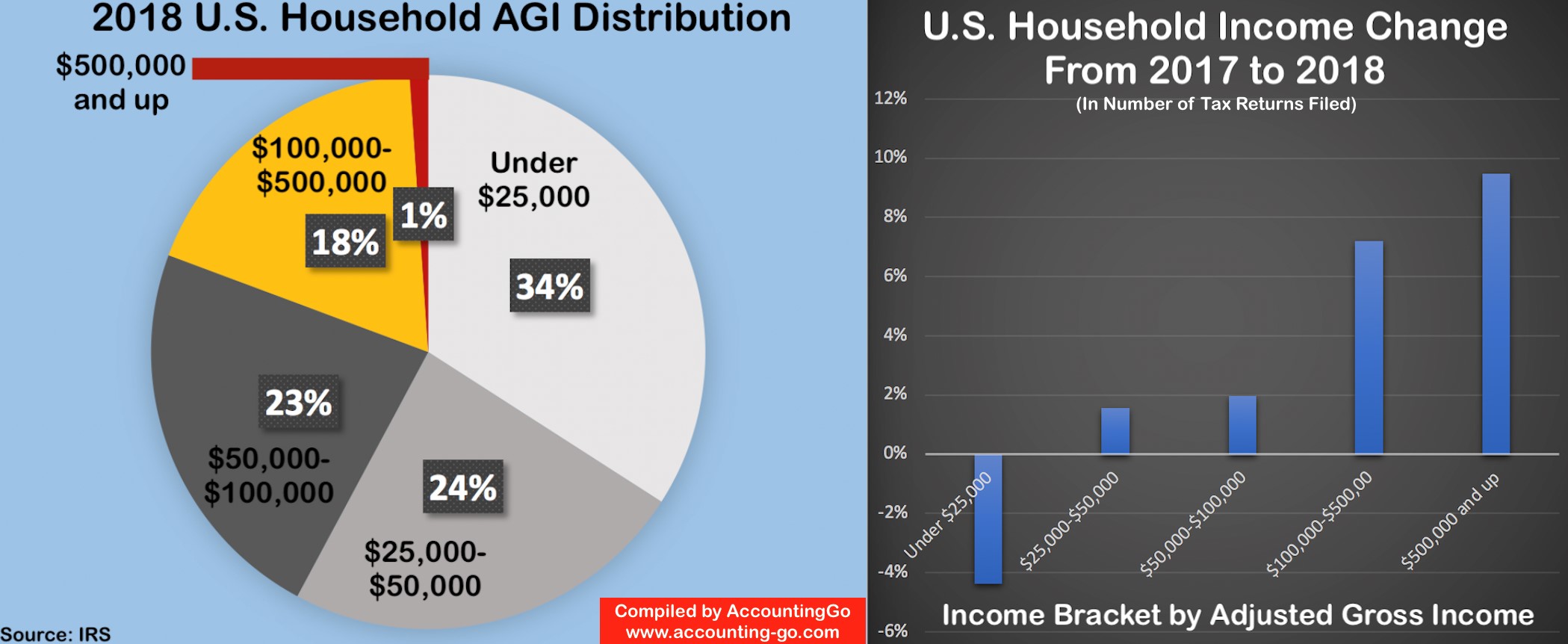

Per the most recent data released from the IRS, there were approximately 153.8 million individual income tax returns filed for year 2018. Of those returns, approximately 58% reported adjusted gross income (AGI) of $50,000 or less, 23% between $50,000 and $100,000, and 19% reported income of $100,000 or more – See the pie chart for more details.

These numbers reflect a big change compared to 10 years ago when 65% of U.S. returns reported an adjusted gross income of less than $50,000 and only 13% of U.S. returns reported an adjusted gross income of $100,000 or more. Although they haven’t been adjusted for inflation.

When comparing 2018 to 2017, the numbers also show a noticeable increase in income reported to the IRS across all income brackets – See the bar chart. The data shows a drop of more than 4% for those making less than $25,000 per year, probably because of the increase in minimum wage in some jurisdictions. The same data shows an increase of more than 7% for those households making between $100,000 and $500,000, and more than 9% for those making more than $500,000. The big increase in the upper-income households was probably because of the appreciation in value of stocks, real estate and other investment assets.

This article can be republished in its entirety with accreditation to AccountingGo and website: www.accounting-go.com

Status of Your Stimulus Payment

Millions of Americans have already received their stimulus payments authorized by the Coronavirus Aid, Relief, and Economic Security Act (CARES Act). The IRS continues to calculate and automatically send the payments to most eligible individuals, however some may have to provide additional information to the IRS to get their payments.

You may be eligible to receive a stimulus payment if you:

– Are a U.S. citizen, permanent resident or qualifying resident alien;

– Cannot be claimed as a dependent on someone else’s return;

– Have a Social Security number (SSN) that is valid for employment (valid SSN); and

– Have adjusted gross income below an amount based on your filing status and the number of your qualifying children.

Exception: If either spouse is a member of the U.S. Armed Forces at any time during the taxable year, then only one spouse needs to have a valid SSN.

To check on the status of your stimulus payment, click here.

For more information, click here

Should you amend your 2018’s tax return?

The Coronavirus Aid, Relief, and Economic Security (CARES) Act was signed into law on March 27, 2020 as part of a $2.2 trillion aid package.

Some parts of the bill do not require you to take any action such as the ‘stimulus check’ for eligible individuals ($2,400 for joint filers, $500 per qualifying child). However, there are several provisions that apply retroactively, that would require actions such as amending previous tax returns, which could result in significant tax refunds for some taxpayers.

Here are two of the retroactively applicable provisions under the CARES Act that we want to bring to your attention:

- The bill temporarily repeals the 80% income limitation for net operating loss deductions for years beginning before 2021. For losses arising in 2018, 2019, and 2020, a five-year carryback is allowed.

- The bill also makes technical corrections regarding qualified improvement property (QIP) applying retroactively to 2018. QIP is now eligible for 100% bonus depreciation. If your business incurred costs on improving a business property and did not deduct all of the costs in 2018, consult with your tax advisor about this provision. Click here to see the full bill.

IRS Tax Payment and Filing Deadline Extended to July 15, 2020 Due to COVID-19

The IRS today issued guidance allowing all individual and other non-corporate tax filers to defer up to $1 million of federal income tax (including self-employment tax) payments due on April 15, 2020, until July 15, 2020, without penalties or interest. The guidance also allows corporate taxpayers a similar deferment of up to $10 million of federal income tax payments that would be due on April 15, 2020, until July 15, 2020, without penalties or interest.

Update: The IRS announced on March 21, 2020 that the federal income tax filing due date is automatically extended from April 15, 2020, to July 15, 2020.

Taxpayers do not need to file any additional forms or call the IRS to qualify for this automatic federal tax filing and payment relief. Individual taxpayers who need additional time to file beyond the July 15 deadline, can request a filing extension by filing Form 4868 through their tax professional, tax software or using the Free File link on IRS.gov. Businesses who need additional time must file Form 7004. Click here to IRS’s website

How To Select Accounting Software for Construction Contractors

There is no one best software for all contractors.

Although QuickBooks is known as the most popular software among the smaller-sized businesses, many contractors are still searching for alternatives. QuickBooks users find the software easy to use and affordable. However mid-size self-perform contractors opt for more expensive software because the software gives them detailed job cost reports that they need.

In searching for accounting software, you have three options:

- Purchase popular commercial software that your competitors use.

- Purchase not-so-popular commercial software.

- Hire a programmer to write software customized to your business.

In most cases the first choice is recommended not only because the popular software has been tested by many users but also because it is easier to find staff that knows how to use the software.

Using popular software helps you lower support cost, maintenance cost, and training cost, which, in many cases, weigh over the cost of the software itself. In selecting accounting software, contractors ought to do a cost/benefit analysis. Below is a list of suggested cost elements that you should consider before deciding to implement new construction accounting software.

Costs associated with implementing new accounting software:

- Software cost

- Hardware cost

- Labor cost for system set-up and installation

- Labor cost for data transferring

- Training cost

- Cost of learning curve

- Cost of interruption of business activities

- Maintenance cost

- Technical support cost (Items 4-9 are “soft costs”)

While software, hardware, installation costs can be easily estimated, the “soft costs”, which sometimes are much greater than software costs, are very often overlooked. The more sophisticated the software is, the more the soft costs are and the more sophisticated software is, the more time required to set up and maintain.

Contractors should decide how much detailed of job cost reports that would be beneficial for their businesses before seeking advices from accountants regarding selecting construction accounting software.

Bookkeeping and Accounting – what are the differences?

Years ago when accounting software for small businesses was not as popular, the roles of a bookkeeper and an accountant were distinctively different.

A bookkeeper typically handles and records daily transactions such as paying bills, creating invoices, collecting payments, making deposits, managing timesheets for payroll, reconciling bank accounts etc. Records kept by a bookkeeper reflect all cash-in, cash-out of a business in chronological order. The process of compiling these records to prepare financial statements and other meaningful reports is, however, referred to as accounting.

Bookkeeping is a critical part of accounting. Without accurate bookkeeping, financial reports will not be accurate. However, good bookkeeping alone may not give you meaningful financial reports. It takes specialized knowledge, skills, and experience to produce variety of financial statements and quality accounting reports.

Now that accounting software for small businesses can produce Balance Sheet and Profit & Loss reports at the press of a button, the line between bookkeeping and accounting is not as distinctive to some small businesses. Regardless, accounting software still needs input from experienced accountants to produce meaningful reports.

To see how a bookkeeper and an accountant would record a transaction differently, let’s take a look at the following scenario:

A business paid $5,000 down payment and agreed to pay $750/month for 36 months to purchase a vehicle. Sales price of the vehicle was $30,000.

A bookkeeper would typically record the $5,000 as a simple entry cash-out for auto expense.

An accountant would record the $30,000 as fixed asset, and also record the total loan balance, principal payment, interest expense and depreciation expense.

Accurate bookkeeping with organized records provides a strong foundation for quality accounting. Quality accounting enables meaningful reports. Meaningful financial reports reveal true profitability, financial position and cash flows of a business. Meaningful financial reports allow business owners and their consultants making insightful analysis and strategic planning accordingly

How long should you keep your tax returns and supporting documents?

In general, the IRS has three years from the due date of the return or the date on which the return was filed, whichever is later, to audit and adjust the return. However, the IRS has six years to audit a return if a person fails to report over 25% of gross income. If a return is not filed, or a fraudulent return has been filed, the IRS can audit records for that tax year at any time.

For tax returns and forms W-2, we recommend keeping them at least 7 years or permanently if you could. Your tax returns provide support in case the IRS contends you did not file a return or filed a fraudulent return. Keep forms W-2 in case you need to prove earnings or Social Security and Medicare contribution to Social Security Administration many years later.

For documents that has future tax relevance such as cost of stocks purchased, IRA contributions, closing documents of your houses, improvement costs of the houses etc., you will need these documents to calculate gains or losses when you sell these assets. We recommend keeping these documents at least 4 years after you sell and report the sold assets on your tax return.

In conclusion, how long you should keep your tax records depends on the future tax relevance of the documents